Your last grocery run felt heavier on the wallet, right? That same cart costs more than last year, and it is not your imagination. How Inflation Affects Buying Power and Savings is simple at the core: prices rise, which erodes the value of money.

Right now, the US annual inflation rate sits near 3.0% as of late 2025, with a recent uptick tied in part to energy. In this guide, you will see simple math for purchasing power, how higher prices push goals farther away, and practical steps to protect your savings without stress. The tone here is calm, practical, and hopeful, because small moves still work.

Inflation 101: Simple meaning, buying power, and why it hits savings

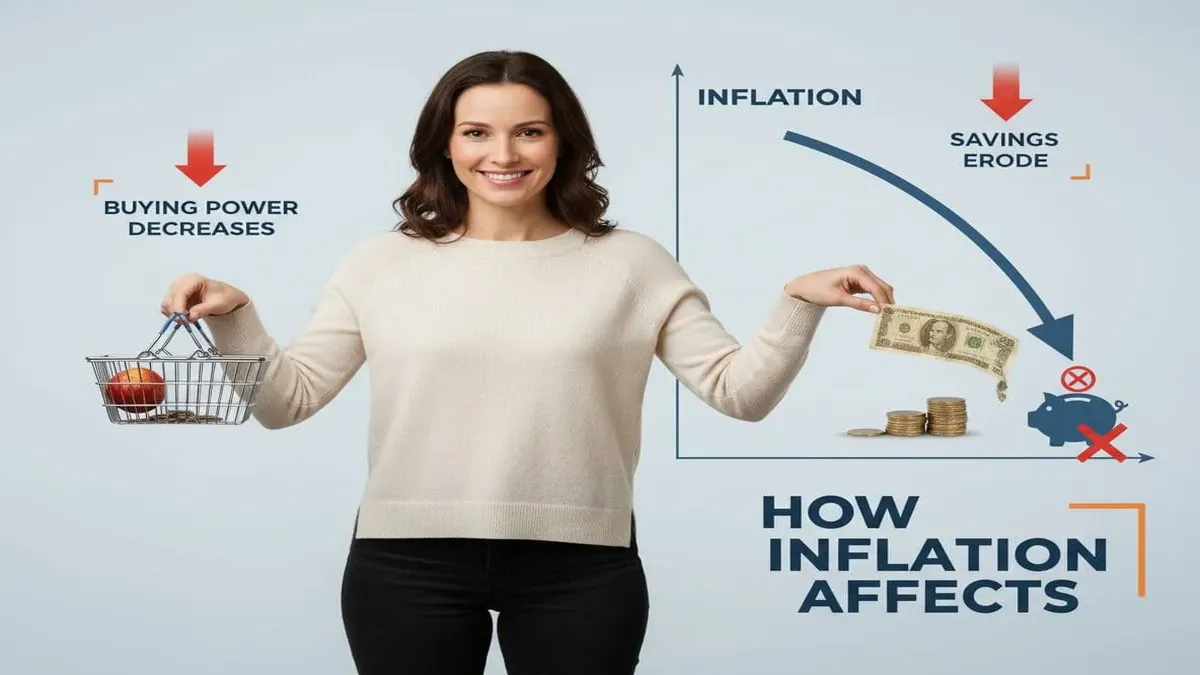

Inflation means price increases go up over time. When prices rise, your money buys fewer goods and services. That is the whole story in one line.

To track price changes, economists use price indexes. The Consumer Price Index, or CPI, measures how much the price of a basket of common items changes each month. It covers things like food, housing, gas, medical care, and more. These indexes turn a messy world of prices into a single number you can follow.

Core inflation removes food and energy from the index. Why remove them? Those prices jump around a lot month to month. Core helps show the trend, not the noise. Both measures matter. Your budget feels what you pay at the pump and the store, and your long-term plan needs a steadier view of price trends.

Nominal returns are the rates you see on savings accounts or investments. Real returns adjust for inflation. If your savings account pays 2%, and inflation is 3%, your real return is negative 1%. The dollars grew, but their buying power shrank.

Think of a $100 budget for school supplies. If inflation is 3%, that same set of supplies may cost $103 next year. If your pay does not rise enough, you buy fewer items or you spend more.

Today’s snapshot: inflation in the US is around 3.0% in late 2025, and energy helped push it up from recent months. For a family, that means a slightly tighter budget unless raises, savings yields, or smart cuts fill the gap. For a clear explainer on savings erosion, see this primer on how inflation impacts savings.

What is inflation? CPI, core inflation, and price indexes in plain words

The Consumer Price Index tracks prices by watching a basket of common goods and services. When the index goes up, it means prices, on average, went up. Core inflation excludes food and energy. Those items can swing fast, so core shows a steadier trend. Both the headline number and core help you see how prices and costs move over time, which is key for planning.

Purchasing Power explained with a $100 example

If inflation is 3%, what cost $100 last year costs $103 this year. Stretch that out, and a slow march of small increases adds up. Think about groceries, school supplies, or a pair of sneakers. A few dollars more each time can push you over your monthly budget unless real wages or savings yields keep pace.

Savings and real return: interest rate minus inflation

Real return equals your interest rate minus inflation. If a savings account pays 1% and inflation is 3%, the real return is negative 2%. Your balance grows in dollars, but not in buying power. A quick mental shortcut helps. The Rule of 72 says you can estimate doubling time by dividing 72 by the rate. At 3% inflation, prices can double in about 24 years. That is why earning more than inflation matters for long-term goals.

What inflation looks like now in the US

As of late 2025, US annual inflation is about 3.0%. It ticked up from around 2.9% in recent months, helped by energy prices, while core inflation sits near 3.0% as well. The takeaway is simple. If your raise or your savings yield trails 3%, your budget feels tighter, and your savings lose ground in real terms. For more on how purchasing power shifts when prices rise, see this short guide on inflation and purchasing power.

What rising prices mean for your budget and big goals

Inflation shows up first in daily life. Groceries, gas, utilities, and streaming bills creep higher. Sometimes the price tag does not change, but the package gets smaller. That is shrinkflation. You pay the same for less.

Higher prices erode your purchasing power and can lower your standard of living. If rates rise to tame inflation, loans and credit can cost more. Adjustable-rate debt, like some credit cards or lines of credit, gets more expensive. Fixed-rate mortgages stay the same, but new loans can be pricier. Rent often adjusts yearly, so renters should expect periodic increases and plan for them.

Big goals also shift. College costs and retirement expenses must be set in future dollars. If your plan uses old prices, the target is too low. That is why saving rates should grow every year. The same is true for emergency funds and cash on hand. If prices rise 3% a year, your cushion should adjust too.

A few quick guardrails help: track a few core staples, audit bills quarterly, maintain an emergency fund, and check that your savings yield is close to inflation or better. For a simple overview of how savings face inflation headwinds and how to respond, see this breakdown on how inflation affects savings.

Everyday costs: groceries, gas, utilities, and subscriptions

Supply chain issues can contribute to shrinkflation, which hides behind familiar brands. A box looks the same, but you get fewer ounces. Price creep shows up on phone, internet, and streaming bills. Track five common items you buy every month to see real changes. Quick wins help: swap brands, buy in bulk for non-perishables, and audit subscriptions each quarter. Cancel what you do not use, then set reminders to review again in three months.

Housing and debt: rent, mortgages, and credit card rates

Rising inflation often leads to higher interest rates on variable debt, so borrowing can get pricier. Fixed-rate loans can protect you, since the payment stays the same as dollars lose value. If you carry credit card balances, pay those down first, since rates there are often high. Keep a payment buffer, like one extra mortgage or rent payment in savings, to cushion surprises. Renters should expect annual increases and budget for them in advance.

Long-term goals: college and retirement savings vs inflation

Inflation raises the target for college and retirement savings. To keep up, raise your contributions at least once a year. Use tax-advantaged accounts when you can, like a 401(k), IRA, or 529 plan. Steady investing beats trying to time the market. If you earn a raise, route a slice to these accounts before it blends into spending.

Emergency funds and fixed incomes: staying above inflation

Aim for a 3 to 6 month cash reserve for living costs. Keep it in a high-yield savings account with no fees and easy access. For retirees or anyone on fixed income, a cost of living adjustment (COLA) is important to help maintain value over time; a mix of cash, short CDs, and a slice of inflation-linked bonds can also cover near-term needs without taking on big risks. Stability matters most for money you need soon.

How to protect buying power and grow savings in an inflation year

Start with a snapshot of your money. List your accounts, rates, and balances. Compare your savings APY to the current inflation rate, which is near 3.0% as of late 2025. If your APY is lower, your real return is negative. That is a nudge to move idle cash.

Next, assign roles to your dollars. Emergency cash stays liquid. Money needed in 1 to 3 years can sit in High-Yield Savings Accounts or a CD ladder. Long-term money belongs in investments that can outpace inflation over time. Automate contributions so you save first, then spend what is left.

Fees matter. Use low-cost funds and simple portfolios. Limit churn. Check in once a quarter, then adjust once or twice a year. That rhythm keeps you focused without bouncing from headline to headline.

Inflation is not a stop sign. It is a speed bump. With the right mix of cash, bonds that adjust to prices, and growth assets, you can keep purchasing power intact while growing your savings. For another clear overview, the Federal resource on the impact of inflation on financial decisions offers helpful basics.

Use high-yield savings and CDs wisely

APY tells you how much your cash earns in a year, including compounding. The goal for near-term cash is to get a rate as close to inflation as possible, or higher if you can. For money you need in 1 to 3 years, a CD ladder can boost yield while staggering maturities. Keep emergency funds in a liquid savings account so you can access cash fast. Check rates every few months and move if a better, no-fee option appears.

Fight inflation with TIPS and I Bonds

TIPS are US Treasury bonds that serve as a hedge against inflation by adjusting their principal with inflation. When prices rise, the principal goes up, so interest payments keep pace. Pro: they help protect buying power. Con: prices can drop when real interest rates rise.

I Bonds are savings bonds with an inflation component that resets twice a year. They have annual purchase limits and tax perks if used for education. Pro: strong inflation protection with federal backing. Con: limited liquidity for the first year and caps on how much you can buy.

For a straightforward overview of purchasing power versus prices, see this clear explainer on the impact of inflation on purchasing power.

Invest for growth: low-cost index funds, stocks, and real assets

Over long periods, stocks through broad index funds have a strong track record of beating inflation. Keep fees low, own a wide slice of the market, and stay invested through ups and downs, considering your risk tolerance. A small allocation to REITs and a modest slice of commodities or precious metals can diversify risk, but they are not core holdings for most people. Use dollar-cost averaging and rebalance once a year to keep these investments on track for long-term growth.

Cut costs and raise income: quick wins that add up

- Negotiate your internet and phone bill every 6 to 12 months.

- Shop your insurance. Bundle or switch if it saves real money.

- Plan meals and batch cook to reduce food waste.

- Sell unused items, then route the cash to your emergency fund.

- Prepare a raise request with market pay data and clear wins.

- Add a simple side gig that fits your schedule.

Automate transfers so savings comes first. When the money moves before you see it, momentum builds.

Inflation FAQs: quick answers people search for

What are the main types of inflation?

Inflation mainly comes in two forms: Demand-Pull Inflation, where strong demand outpaces supply and drives up prices, and Cost-Push Inflation, where rising production costs like wages or materials get passed on to consumers.

What happens to Purchasing Power during inflation?

Prices rise, so each dollar buys less. At 3% inflation (as measured by CPI; economists also use PCE as an alternative), something that cost $1 last year costs about $1.03 this year.

How does inflation impact savings?

If your savings interest rate is below inflation, your real return is negative and your savings lose buying power. The simple formula is real return equals interest rate minus inflation.

Is any inflation good for the economy?

Low, steady inflation can support growth because it encourages healthy Consumer Spending and investment by people and businesses. Deflation is harmful, as it leads to delayed purchases and can spiral into economic stagnation. Very high inflation hurts planning and budgets.

What is the role of the Federal Reserve?

The Federal Reserve, often called the Fed, uses Monetary Policy to manage the Money Supply and keep inflation in check, aiming for a target around 2% to promote stable growth.

How can I protect savings from inflation?

Use high-yield savings for cash needs, consider TIPS or I Bonds, invest long term in low-cost index funds, and keep costs low. The Fed’s influence on interest rates can help boost yields on these options. The core idea is How Inflation Affects Buying Power and Savings, so aim for real returns that meet or beat inflation.

Conclusion

Rising prices reduce what money can buy, so plan for real returns that clear inflation. Next steps: check your savings APY, set auto increases for Retirement Savings, review debt rates and pay down high-interest balances, build or top up a 3 to 6 month cash buffer, and add an inflation fighter like TIPS or I Bonds. With inflation sitting near 3.0%, a few focused moves can steady your budget and keep long-term goals on track. Small changes, repeated, become big wins over time. Stay consistent, and you will protect Purchasing Power while growing savings, even in a year shaped by How Inflation Affects Buying Power.