Want to keep more of every dollar you invest? In 2025, U.S. rules still reward smart planning, and tax-efficient investing for your retirement portfolio means using the right accounts, asset placement, and withdrawal order to cut lifetime taxes. Put simply, it is about paying less tax over time, not just this year.

Here is what you will get. We will compare tax-advantaged accounts like 401(k), IRA, Roth, and HSA, and show where each shines. We will cover asset location, which assets fit best in each account, plus Roth conversions to build tax-free income later. You will also see how to handle RMDs and use QCDs to lower taxes while giving to charity, including a tax-efficient withdrawal strategy to minimize lifetime taxes.

By the end, you will have a simple action plan you can start this year. Small moves, like where you hold bonds or when you convert to Roth, can add up. You worked hard for your savings, now let taxes take less.

What Tax-Efficient Investing for Retirement Portfolios Means in 2025

Tax-efficient investing is placement, timing, and smart choices that cut taxes over decades. In 2025, rules still reward you for thinking ahead: 401(k) limits are higher, and Roth rules continue to shine. The payoff is simple, higher after-tax returns, more flexibility, and less stress when you need income. We use topic / title as primary keyword to keep this guide consistent and easy to find.

Tax-efficient investing is placement, timing, and smart choices that cut taxes over decades. In 2025, rules still reward you for thinking ahead: 401(k) limits are higher, and Roth rules continue to shine. The payoff is simple, higher after-tax returns, more flexibility, and less stress when you need income. We use topic / title as primary keyword to keep this guide consistent and easy to find.

Think of it like packing a suitcase. Put the heavy stuff where it fits best, keep essentials handy, and plan for changing weather. Your accounts work the same way. Choose where to place assets, when to realize income, and how to draw cash in retirement so taxes take less.

Taxes can eat returns faster than you think

Yearly taxes reduce compounding. Say you hold a taxable bond fund that yields 5 percent. At a 24 percent tax rate, you keep 3.8 percent each year. On $100,000, after 20 years you get about $212,000. If that same bond fund sits in a tax-deferred account, it compounds at 5 percent without yearly tax drag, growing to about $265,000 before any withdrawals. That gap, around $53,000, is the cost of taxes hitting you every year instead of later.

Short-term capital gains and high-turnover funds make the drag worse, since they throw off more taxable income. Move interest-heavy or holdings with high portfolio turnover into IRAs or 401(k)s when you can. Keep broad, tax-friendly index funds in taxable. Small placement choices today improve what you keep tomorrow.

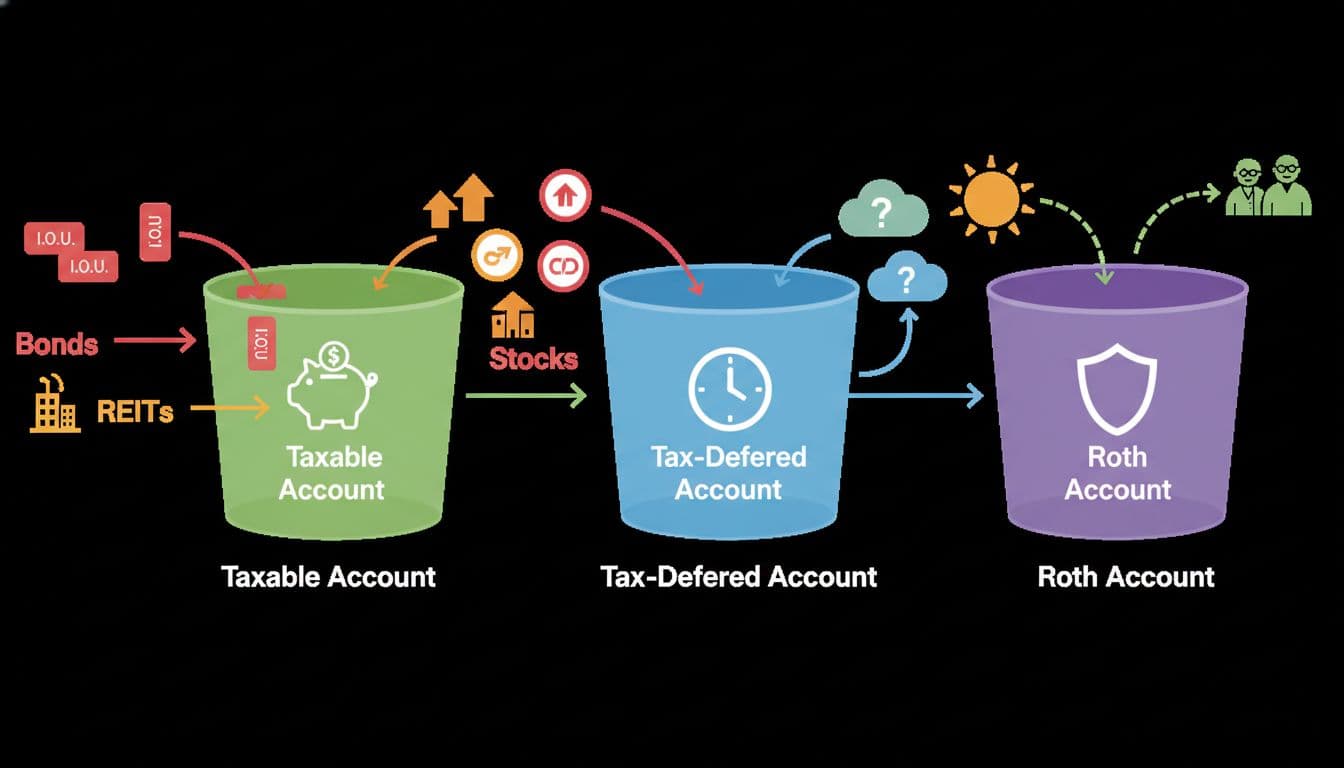

The three tax buckets you need for flexibility

– Taxable accounts: Taxable brokerage accounts that you can tap anytime. You pay taxes on dividends, interest, and realized gains as you go. Use them for flexibility and long-term index funds with low turnover.

– Taxable accounts: Taxable brokerage accounts that you can tap anytime. You pay taxes on dividends, interest, and realized gains as you go. Use them for flexibility and long-term index funds with low turnover.

- Tax-deferred accounts: Traditional 401(k)s and IRAs. Money grows without yearly taxes, but withdrawals are taxed as income. Great for bonds and strategies that would be tax-inefficient in taxable.

- Tax-free: Roth IRAs and Roth 401(k)s. Qualified withdrawals are tax-free. Ideal for high-growth assets and future spending flexibility.

Why hold all three? You can pull from the best bucket each year to keep your tax rate in a sweet spot. Low-income year, tap pre-tax. High-income year, spend from Roth or taxable basis. This tax diversification also protects you from future tax changes, since you are not locked into one tax outcome.

Key 2025 rules to keep on your radar

A few updates matter for planning this year. Keep these in your back pocket:

- RMDs generally begin at age 73 for many savers. See the IRS FAQ for timing details in different situations at the IRS RMD FAQs.

- 401(k) employee deferral limit is $23,500 for 2025.

- Catch-up contribution is $7,500 from age 50.

- QCDs from IRAs are allowed starting at 70½. Learn how they can reduce taxable income at Fidelity’s overview of Qualified Charitable Distributions.

- Roth IRA and Roth 401(k) withdrawals can be tax-free if you meet the rules, usually age 59½ and a 5-year clock.

These are small moves with big impact when used together.

Common mistakes that raise your tax bill

Avoid easy errors that compound over time:

- No tax diversification: Holding only pre-tax accounts leaves you fewer choices later.

- Ignoring required distribution planning: Delaying all pre-tax withdrawals can push you into higher brackets in your 70s.

- Placing high-turnover funds in taxable: This creates avoidable yearly taxes. Put them in IRAs or 401(k)s.

- Skipping rebalancing: Letting winners run in taxable can set up large future gains. Trim steadily and use new cash to rebalance.

- Large Roth conversion in one high-income year: Spreading conversions over several years often reduces total tax.

Small adjustments now can lower lifetime taxes and raise what you get to spend in retirement.

Pick the Right Accounts in 2025 to Cut Lifetime Taxes

401(k) and Traditional IRA: reduce taxes today, grow tax-deferred

Tax-deferred accounts like these offer pre-tax contributions that cut your taxable income this year, then provide tax-deferred growth without yearly taxes. You defer the tax bill until withdrawals, which are taxed as ordinary income. This can help if your tax rate is lower in retirement.

For 2025, employees can defer up to $23,500, with a $7,500 catch-up at age 50 and older. See current details on contribution limits. Aim to capture your employer match first. That match is free money that compounds for you.

Use these options when a workplace plan is not available or when a deduction fits your bracket. High interest or high-turnover holdings often belong here, since tax-deferred growth shields you from annual tax drag. Later, plan withdrawals to stay within target tax brackets and to manage required minimum distributions.

Roth IRA and Roth 401(k): tax-free growth and smart conversions

Roth accounts use after-tax contributions. Qualified withdrawals are tax-free if you meet the age and 5-year rules. That tax-free pool gives you powerful control over future income.

A Roth conversion moves money from pre-tax to Roth, and you pay tax in the year of the move. Converting in lower-income years, or before RMDs begin, can reduce lifetime taxes while helping manage your tax bracket. Many investors use partial conversions to “fill” lower tax brackets each year instead of doing one large conversion. This spreads the tax hit and smooths your future RMDs. Want a framework to evaluate this move? See practical strategies in Schwab’s guide on

Asset Location: Put the Right Investments in the Right Accounts

Asset location is simple. Place each asset in the account type that gives the best after-tax result. Done well, it can lift long-term after-tax returns without extra risk through tax-efficient investments. For use topic / title as primary keyword, follow a few rules of thumb and keep a clean map you can maintain. For a helpful primer, see Fidelity’s overview on asset location and lower taxes.

Asset location is simple. Place each asset in the account type that gives the best after-tax result. Done well, it can lift long-term after-tax returns without extra risk through tax-efficient investments. For use topic / title as primary keyword, follow a few rules of thumb and keep a clean map you can maintain. For a helpful primer, see Fidelity’s overview on asset location and lower taxes.

Hold bonds and REITs in tax-deferred accounts

Bond interest and most REIT distributions are taxed as ordinary income tax. That higher tax rate makes them better fits inside a Traditional IRA or 401(k), where earnings grow tax-deferred in tax-deferred accounts. This placement cuts annual tax drag and keeps more compounding working for you.

If you run out of tax-deferred space, a few exceptions can help. In taxable, consider high-quality municipal bond funds if your tax bracket is high. You can also use Treasuries, which may be exempt from state income tax. For REITs, keep positions modest in taxable, and favor funds with lower turnover to limit surprises at tax time. The goal is not perfection, it is better average placement over many years. T. Rowe Price explains why this split matters in their guide on asset location and tax-efficient investing.

Keep broad index funds and ETFs in taxable accounts

Broad index funds and ETFs tend to have low turnover. That means fewer taxable distributions. Many stock index funds also pay qualified dividends, which get lower tax rates as long-term capital gains in taxable accounts. You also control when to sell, so you decide when to realize capital gains.

For simplicity, pick a total U.S. market fund, a total international fund, or an S&P 500 fund in taxable accounts. ETFs are especially tax efficient due to their structure. Use specific-lot tracking and only sell what you need. Pair this with tax-loss harvesting when the market pulls back to offset gains from rebalancing or other sales, using capital losses to your advantage (just mind the wash sale rule that disallows claiming losses on repurchased securities within 30 days). Keeping core stock index funds in taxable gives you flexibility and keeps yearly taxes in check.

Use Roth space for assets with big growth potential

Roth accounts shine for long-term growth. Qualified withdrawals are tax-free if you meet the rules. That makes them ideal homes for assets with higher expected growth, like small-cap funds, quality growth stocks, or a satellite international sleeve.

You still need a risk budget. High-growth assets can swing a lot, and a Roth is not a magic shield against market drops. Keep position sizes sane, diversify, and match your time horizon. The prize is that future gains and withdrawals can be tax-free, so every extra point of growth in a Roth can be worth more to your retirement spending power. When in doubt, place the highest expected return assets in Roth, not the most speculative.

A simple asset location map for a 60/40 or 70/30 portfolio

Here is a practical template you can tailor:

- Traditional IRA or 401(k): all core bonds first, then REITs.

- Taxable brokerage: broad stock index funds, like total market or S&P 500, plus total international.

- Roth IRA or Roth 401(k): higher-growth slices, such as small-cap, factor funds, or a select growth stock sleeve.

Example mix for 60/40: fill 40 percent bonds and any REITs in pre-tax accounts, hold most of the 60 percent stock index in taxable, and put a 10 to 20 percent slice of the stock mix with higher growth potential in Roth. For 70/30, apply the same map, just less bond space.

Rebalance with new cash and dividends first to limit taxes. Then trim in tax-deferred or Roth when possible, and only sell in taxable when needed.

FAQs: People Also Ask on Tax-Efficient Investing for Retirement Portfolios

Quick answers to the top questions investors ask, designed to help you keep more of your returns. For added context on tactics that reduce tax drag, see this clear overview from Morgan Stanley on tax-efficient investing.

Quick answers to the top questions investors ask, designed to help you keep more of your returns. For added context on tactics that reduce tax drag, see this clear overview from Morgan Stanley on tax-efficient investing.

What is tax-efficient investing?

Tax-efficient investing means structuring your accounts, asset location, and withdrawals to reduce taxes and raise your after-tax returns. You pick the right assets for each account, then plan tax-smart withdrawals and how to take income. Example: hold bond funds in a Traditional IRA to shield interest from yearly taxes, keep broad stock index ETFs in taxable for lower distributions, and use Roth for higher-growth slices. In this section, we use topic / title as primary keyword to reinforce the core idea.

Should I convert my Traditional IRA to a Roth IRA?

It depends on your current tax rate versus your expected future rate, your time horizon, and RMD planning. Conversions make sense when you can pay the tax from cash and expect higher rates later, or want tax-free withdrawals for flexibility. Many investors convert in stages. Use partial conversions in lower-income years, or before RMDs start, to fill lower brackets without jumping to a higher tax bracket. Map conversions to your long-term bracket targets, not just this year; this approach can also help manage the taxation of Social Security benefits by controlling your overall income levels.

How does asset location improve tax efficiency?

Placing tax-inefficient assets in tax-deferred accounts, and tax-efficient assets in taxable accounts, reduces yearly tax drag and boosts compounding. Interest from bonds and ordinary REIT income fits well in Traditional IRAs or 401(k)s, while low-turnover stock index funds belong in taxable. Example: put core bonds in your 401(k), and keep a total market ETF in taxable so you control when gains are realized. This split can add meaningful after-tax growth over decades.

What accounts should I use to save for retirement?

Use a mix of taxable, tax-deferred, and tax-free accounts for flexibility and lower lifetime taxes. Prioritize workplace plans like a 401(k), then Traditional or Roth IRAs based on your bracket, and add an HSA if eligible for triple tax benefits. Tax diversification lets you choose the right bucket each year. For a simple checklist on spreading savings across account types, see Nationwide’s 2025 guide on tax-saving considerations.

Conclusion

Keep more of every dollar by sticking to the big wins. Pick the right accounts, place assets where they are most tax-friendly, follow a tax-efficient withdrawal strategy, and keep steady yearly habits. That is how tax-efficient investing for your retirement portfolio turns into higher after-tax income and less stress when markets shift.

Act this week. Check your contribution levels and capture every match. Review asset location so bonds and REITs sit in tax-deferred, broad stock index funds stay in taxable, and your best growth lives in Roth. Plan a small Roth conversion to fill a lower bracket. Set calendar reminders for RMDs and QCDs so dates never sneak up on you.

Your money deserves intention, not autopilot. Simple, repeatable steps beat complex moves you never finish, and incorporating estate planning ensures long-term security for your legacy. If you want one note to pin to your desk, write this: use topic / title as primary keyword. Thanks for reading, and share the move you will take today.